DEMOCRATIC REPUBLIC OF CONGO (DRC)

Katanga Mining Ltd (KML)

Kamoto Mining project

The project has come under intense criticism in Congo, Belgium, the UK and Canada, because it is thought to be pillaging the resources of DRC, as well as for alledged bribery and corruption. See these critics in the left frame,  particularly this one from a congolese source; and this one from Mining Watch Canada.

particularly this one from a congolese source; and this one from Mining Watch Canada.

Those in favour of the project argue that the agreement has been reached in accordance with the mining law of 2002, that GCM's interests have been preserved, that the projet will give employement to 12 000 and their families and sustain activity for 240 000 people. See these arguments in the praise links of the left frame. Of which this one which denounces international NGO's including RAID UK. And this one GAForrest's address on the day of official transfer of GCM's facilities to Kamoto Copper Company.

So what is the problem?

In accordance with the agreement signed with Gecamines (GCM), KML have undertaken a feasibility study of the project. A "Technical Report" with an economic analysis has been produced which shows sources and uses of funds over the 20 year life of the project. A definitive feasibility report for project implementation is presently underway.

I have no intention to question the "Technical Report" which has been performed by a multi-disciplinary team of reputed mining and metallurgical experts independently of KML. Their work appears to have been done according to the state of the art, in particular, for geological reserve estimates - in the categories of certainty: measured, proven, inferred, and probable - cut off grades have been established to quantify economically recoverable reserves, underground mining plans are made according to professional standards, openpit distribution of grades have been established using geostatistical methods, ultimate pit configurations have been drawn based on the computed cut-off grades and 3 dimensional block modelling... This work is professional without doubt. Of course there are always elements that can be questioned and that are subject to debate between geologists, mining and metallurgical specialists. But such questioning is out of the scope of this essay. I shall therefore use the data of this Technical Report.

I wish to concentrate on the economic aspects of the project in order to assess if the interests of Gecamines and therefore of the local communities and of Katanga and DRC are taken care of in fairness.

With the capital and operating cost estimates given in the Technical Report, and copper/cobalt prices cif ex Durban RSA to Europe/US/China/Corea/Japan of 1.1/10 US$/lb, the internal rate of return of the project, the IRR, is 32.7%%. This IRR is high, if it is referred to the opportunity cost of capital in developed countries of 4% in constant money value (6% in current) because it leaves a margin of 28.7%. But in DRC the opportunity cost of capital carries a risk factor. This is estimated as 8% in constant money value. So the opportunity cost of capital in RDC is taken as 12%. Then the base case IRR for the project sponsors, with the data considered, is 16.7% above the opportunity cost of capital of 12%. This produces revenues for developing other mines, or investing in other industrial projects in RDC and in other parts of the world. This rate of return is shared between the project owners, ie. KML and Gecamines at 75% and 25% respectively, within a Joint Venture SARL ie. KCC (Kamoto Copper Company). KCC was created in order that Gecamines could transfer its properties to a private company that could enter into an agreement with a foreign partner. See details on this.

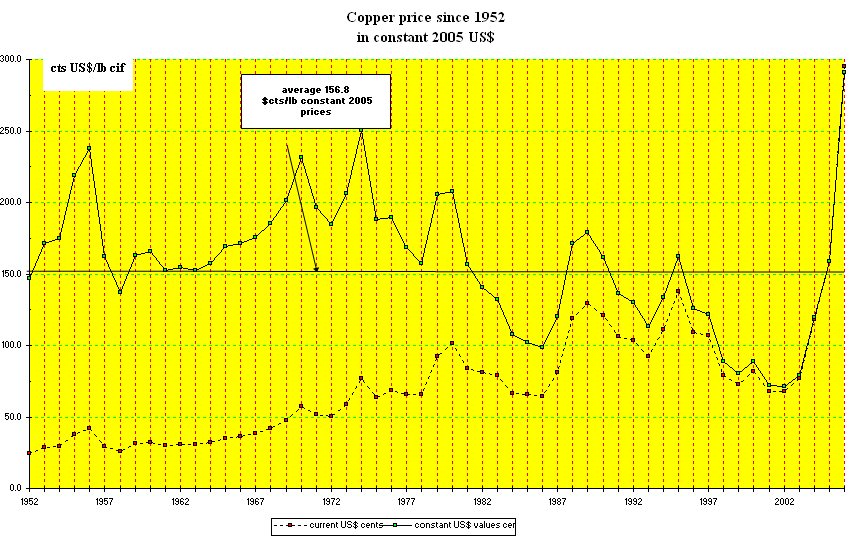

Cu and Co pricesThe 53 year average price of copper in constant $/lb is 1.57$/lb in 2005 prices.  See historic trend. Recent trends have seen a dramatic increase of copper prices due to growth of demand fast developing China and India.

See historic trend. Recent trends have seen a dramatic increase of copper prices due to growth of demand fast developing China and India.  See prices 11/1998-11/2006 in current US$/mt values. In 2006 average transactions at LME were 2.5$/lb Cu.

See prices 11/1998-11/2006 in current US$/mt values. In 2006 average transactions at LME were 2.5$/lb Cu.

The historical price of Co over the same period is 15$/lb 100>% Co content.  See historical price Co 1952-2004.

See historical price Co 1952-2004.

The copper and cobalt prices of 1.10 US$/lb and 10.0 US$/lb considered in the Technical Report are therefore conservative; very conservative as the average Cu price 1952-2005 in 2005 US$ is 1.57 US$/lb and the average Co price is 15$/lb. This leads to my second question.

early stages of negotiation.

GCM's share depends on the value that is attached to the assets transferred by Gecamines to the JV company KCC ie. geological reserves measured and proved, and existing plant and equipment, as this value affects the additional capital required for refurbishing. See existing assets. Depending on the book value of the assets, the share may lie between the present 25% and a desirable 49%. The value of the assets is reflected in KML's project overview.

The issue should be to amend GCM's share if it is undevalued rather than to disrupt the whole project and start the procedure afresh, a process which would take a lot of time. I assume that KML is in earnest with regard to the project. This is apparent by the fact that all data are public in KML's web site. And also if one reads Georges Arthur Forrest's address to the locals on the occasion of the official transfer of GCM's facilities to the joint venture company SARL KCC Kamoto Copper Company. This document is proof that KML takes, publicly, officially and solemly, definite engagements towards DRC, Katanga, Kolwezi and its population, with regard to the social and financial impacts of the project for them.

I therfore assume that there is possibility to amend the agreement if it is found unfair and/or leonine. See article on this.

The approach I use is the following. On the basis of the technical data and the cost estimates therein, I have developed an excel sheet to calculate the internal rate of return of the project. The IRR is the rate of interest that makes nil the 20 year schedule of gross cahflow:

gross cashlow = sales - capital investments - direct operating costs.

See a course on economic evaluations of mining projects, of which this  diagram on the flow of cash.

diagram on the flow of cash.

Note: I have made an adjustment to the so called "DRC benefits" of the Technical Report. The report lists direct costs and indirect costs eg. royalties, taxes on income and dividend tax. The two latter costs have been discarded in my assessement of the IRR.  See these data. And I have a question on General and Administration (G&A) costs and transport costs; do G&A costs include transport costs, in which case, transport costs may have be counted twice?

See these data. And I have a question on General and Administration (G&A) costs and transport costs; do G&A costs include transport costs, in which case, transport costs may have be counted twice?

This being said, my approach is identical to the method followed by Kalala

in his report of september 2006; but the figures adopted by Kalala are now superseded by the data of the Technical Report. Kalala's questions on the leonine character of the mining agreement remain valid, but with different quantitative arguments. I shall therefore not use Kalala's data. See extract of this report relating to Kamoto.

The Technical Report is made within a framework of KML undertaking the project alone. If this project was built from grassroots, or if they were privatised, the existing assets of GMC or assets sold, would have to be created or acquired, and this would significantly increase the initial capital cost and reduce the IRR. The present worth value of GMC may be small or negative in monetary value according to GMC's consolidated accounts; but for KML, the physical assets ie. Cu/Co reserves, all plant and equipment transferred by GCM to KCC are real. The age and capacities of the of the installations are given in KML's website. See this again.

As these assets are not valued in the Technical Report, the IRR is higher than it would be, due to this. The 75/25% equity share in KCC between KML/GMC has to be taken into consideration and valued in an IRR assessement. GMC's entitlement to a 25% owner's equity share should correspond to a value of "acquisition of GMC's existing assets" which can be estimated. See GCM's existing assets.

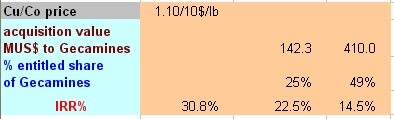

I have therefore made a provision in the model, for an "acquisition value" of the assets transferred by GCM to KCC, which corresponds to the price that a buyer would have to pay for those existing assets, thereby adding to the investment costs. The existing assets are listed as follows in the "Technical report". The "acquisition value" is calculated on the basis of the share of total capital cost of the project, and this is assumed to be share of owners' (KML+GCM) equity; hence, the IRR is reduced. The base case as calculated from the Technical Report's data is taken with an "acquisition value" of zero despite the fact that GCM's share of owner's equity is 25%, and Cu/Co prices of 1.1/10$/lb. This gives a base IRR of 30.8%, shared 75/25% between KML and GCM.

The model (an excel sheet) can be accessed by clicking on this link.

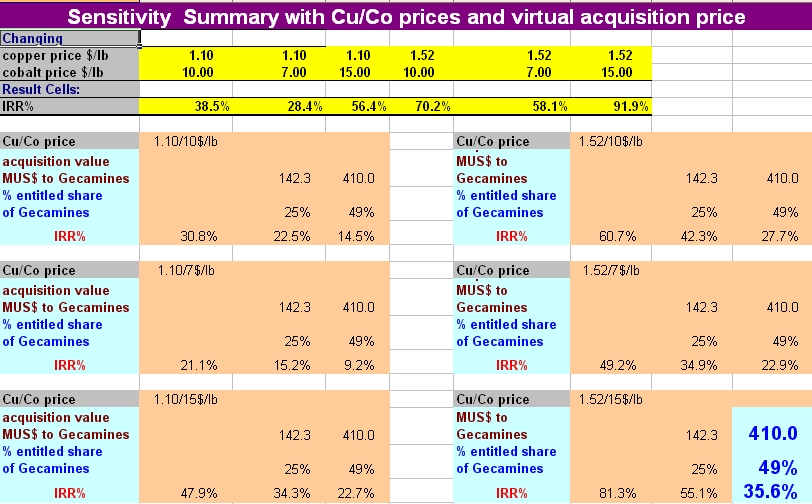

Having developed this model, I have built a sensitivity sheet in the excel table.

Sensitivity to the "acquisition price" ie. GCM's share of owner's equity can first be established. The results are as follows for the base case ie. with Cu/Co prices of 1.1/10US$/lb:

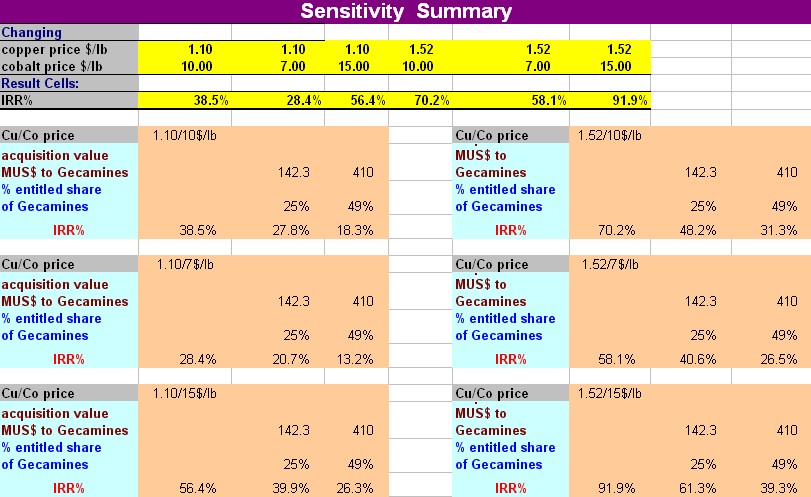

See summary of this base case.See summary of this base case.

See summary of this base case.See summary of this base case. See summary of this scenario.

See summary of this scenario. in this excerpt of the excel sheet.

in this excerpt of the excel sheet.

In view of this, the remaining question for justifying an amendment to the contract GCM/KCC/KML is "what is the real value of assets transferred to KML by GCM?" according to their book value in the accounts, their physical state and capacity to resume operations, and allowing for a reasonable discount... If this value could be obtained, it would further strengthen the case of what the fair share of owner's equity should be for GCM, at least the right of veto. It is indeed desirable that GCM have right of veto so that their responsibility and accountability are engaged in the process for the future. By comparison Balkashmed copper complex in Kazakstan was estimated at an acquisition price of 450 MUS$ for 150 000mt Cu per year at 0.90 US$/lb. That is 3 000 US$ per tonne of Cu. With 115 000t Cu and 6 000t Co, an equivalent 150 000t Cu at 1.1/10$/lb prices, the acquistion price should be of the order of 450 MUS$. The quality of the assets are shown in the november 2006 report of KML on the advancement of the project.

A summary table of these sensitivity calculations is given in a separate sheet of the excel table.  See this summary.See full calculations in html format.Or download kamoto.xls.

See this summary.See full calculations in html format.Or download kamoto.xls.

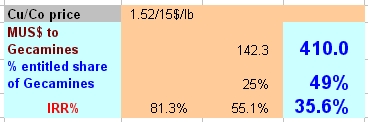

With the data of the Technical Study of KML, with all data that are provided in their website, plus everything else that can be viewed on the net, including your own data, I have built an economic model of the project to show the Internal rate of return, of the cashflow generated by sales of Cu/Co (cif European ports eg. Rotterdam) less direct costs of operation. With a price of Cu of 1.52$/lb which the average price during the period 1952-2005 in 2005 US$ value and a price of Co of 15$/lb also the average Co price during the period 1952-2005 in 2005 US$ value, a production of 115000t Cu and 6000t Co, the IRR is 81.3% which can be referred to an opportunity cost of capital 12%.

The project is run by a joint venture KCC, with holdings of 75%/25% to KML and GCM respectively. To assess the effect of 25% equity share held by GCM, a virtual acquisition cost of physical assets transferred from GCM to JV KCC has been calculated. This is a value which, if it were counted as initial capital, would represent 25% of total capital cost ie. capital required to refurbish plant and equipment by KML, plus a virtual acquisition price to GCM. This calculation yields a virtual acquisition price of 142.3 million US$ and an IRR of 55.1% which would remain for to KML alone if the acquisition price was paid instead of giving GCM 25% equity share.

In view of the assets transferred by GCM to KCC, of their description by KML, of pictures shown on their website, and of my experience of similar projects in Kazakstan, Peru and the Urals, 142.3 million US$ seems very small indeed; the more so if geological reserves are counted in the degree of certainty measured and proven which reflects costly exploration work done by GCM before the transfer.

I have therefore calculated by sensitivity, what virtual acquisition price would correspond to 49% equity share for GCM. This amounts to 410 million US$ and an IRR of 35.6% which would remain for to KML alone if the acquisition price was paid instead of giving GCM 49% equity share. 35.6% is 23.6% above the opportunty cost of capital, with DRC risk factor included, of 12%.

The question now is to negotiate a modified equity share for GCM between 25% and 49%; and to strengthen the case, what is the actual value of assets transferred by GCM to KCC compared to 410 million US$. If it is greater, which I would suspect, 410 million US$ is a discounted value and the % of discount would be a strong argument for 49%.

The only way to obtain to obtain actual value of assets transferred by GCM to KCC is to visit the site and to run a technical and financial audit of the assets and accounts.

Read further thoughts on the necessity to renegotiate the agreement between KML and KCC.

Updated on 01/02/2007 by Pierre Ratcliffe Contact: (pratclif@free.fr) web site http://pierreratcliffe.blogspot.com